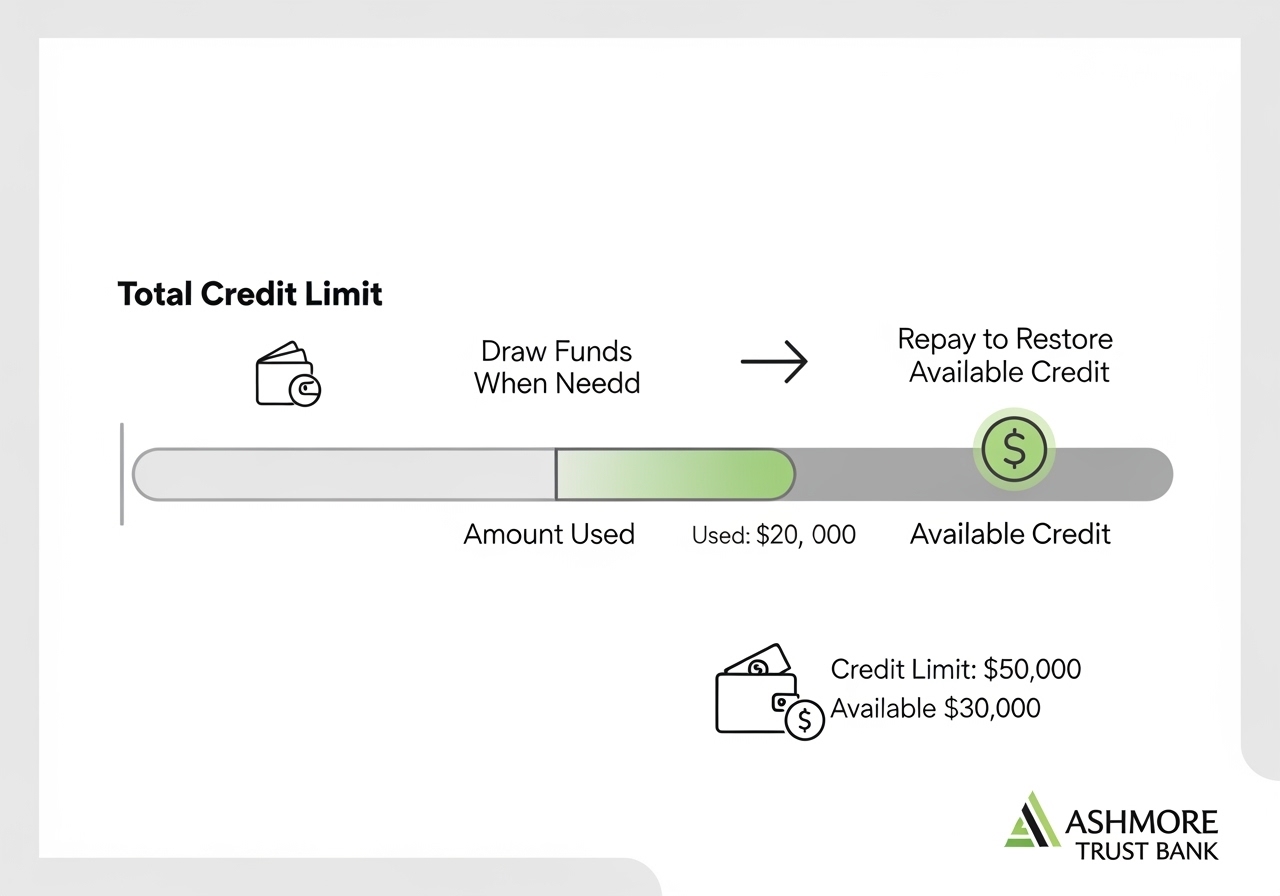

Flexible Business Lines of Credit

Access funds when you need them with a revolving line of credit. Perfect for managing cash flow, seasonal inventory, and unexpected opportunities.

7.49%

APR Starting At

$250k

Maximum Credit

Interest

Pay Only on What You Use